بِسۡمِ اللهِ الرَّحۡمٰنِ الرَّحِيۡمِ

وراثتی قرضوں کے حل کے لیے مقامی کمیٹی کا قیام

اردو ترجمہ کے لیے نیچے سکرول کریں۔

This is a proposal for local Muslim burial councils, Councils of Mosques, and individual Masājid to consider establishing an "Inheritance Debt Resolution Committee" to facilitate the expeditious settlement of debts owed by deceased individuals. The proposed Committee would address several key issues in the current process of debt resolution in Muslim communities.

Please note this is a draft proposal. Any constructive comments or suggestions are welcome via the website or via email to ahussain1999@doctors.org.uk

Introduction

Debt in Islam is not merely a financial obligation but a profound moral responsibility. The Prophet Muhammad (![]() ) informed us that, “The soul of a believer remains suspended until their debt is settled” (Tirmidhi, Book 7, Hadith 49) and he (

) informed us that, “The soul of a believer remains suspended until their debt is settled” (Tirmidhi, Book 7, Hadith 49) and he (![]() ) said, “In matters of debt. By Him in whose hand Muhammad’s soul is, if a man were to be killed in God’s path then come to life, be killed again in God’s path then come to life, and be killed once more in God’s path then come to life owing a debt, he would not enter paradise till his debt was paid.” (Ahmad transmitted it, Mishkat al-Masabih 2929). This spiritual urgency underscores the Islamic mandate to resolve debts promptly, ensuring the deceased’s peaceful transition to the Hereafter. The Quran further mandates documentation of debts: “When you contract a loan for a fixed period, commit it to writing” (Quran 2:282), establishing transparency as a divine principle.

) said, “In matters of debt. By Him in whose hand Muhammad’s soul is, if a man were to be killed in God’s path then come to life, be killed again in God’s path then come to life, and be killed once more in God’s path then come to life owing a debt, he would not enter paradise till his debt was paid.” (Ahmad transmitted it, Mishkat al-Masabih 2929). This spiritual urgency underscores the Islamic mandate to resolve debts promptly, ensuring the deceased’s peaceful transition to the Hereafter. The Quran further mandates documentation of debts: “When you contract a loan for a fixed period, commit it to writing” (Quran 2:282), establishing transparency as a divine principle.

Inheritance debt refers to debts left behind by a deceased person that must be settled from their estate before the remaining assets can be distributed to heirs. In Islamic law, settling the debts of the deceased is considered a critical obligation that takes precedence over distributing inheritance.

Establishing a local Inheritance Debt Resolution Committee (IDRC) aligns with these teachings, offering a structured mechanism to address unresolved debts. By centralising efforts under Islamic institutions, the IDRC would uphold communal accountability, mitigate familial disputes, and fulfil the Quranic injunction to “cooperate in righteousness and piety” (Quran 5:2).

Scope and Importance of the Problem

Over 56% of UK adults die without a valid will, complicating inheritance distribution. Within Muslim communities, informal lending practices exacerbate this issue: many transactions lack written documentation, contravening Quranic directives. Undocumented debts leave families unaware of liabilities, risking violations of Islamic inheritance laws (Quran 4:11–12).

The consequences are severe. Creditors face uncertainty, while heirs risk inheriting unresolved liabilities. The Prophet (![]() ) emphasised communal responsibility, refusing to pray over a debtor until a companion settled the debt (Musnad Ahmad 3/629). Without a systematic resolution, the deceased’s soul remains in spiritual limbo, and families endure prolonged financial and emotional strain.

) emphasised communal responsibility, refusing to pray over a debtor until a companion settled the debt (Musnad Ahmad 3/629). Without a systematic resolution, the deceased’s soul remains in spiritual limbo, and families endure prolonged financial and emotional strain.

Proposal to Tackle the Problem

A proposal s made in this paper to establish local Inheritance Debt Resolution Committees (IDRC) under the auspices of the local Council of Masasjid in collaboration with local Muslim Burial Council (local MBC) and local imams. This collaborative initiative would try to ensure the debts of all locally deceased Muslims is settled expeditiously while being deeply rooted in community structures and religious authority, enhancing its credibility and reach.

The IDRC's primary objectives would be threefold, each addressing a critical aspect of Islamic financial ethics and inheritance practices. Firstly, the Committee would spearhead efforts to encourage Muslims to formalise their debts through written contracts. This documentation drive aligns with Quranic injunctions to record financial transactions, as stated in Surah Al-Baqarah (2:282), promoting transparency and reducing potential disputes.

Secondly, the IDRC will focus on educational initiatives, organising workshops and seminars to promote understanding of Islamic inheritance laws and the importance of writing an Islamic Will which is valid under English law. These educational efforts aim to address the alarming statistic that over 56% of UK adults die intestate, a figure potentially higher among Muslim communities due to misconceptions about Sharia compliance in UK inheritance laws.

Thirdly, the committee could serve a mediatory role, acting as an intermediary between creditors and bereaved families. This function is particularly vital in navigating the sensitive period following a death, ensuring that debt claims are handled with both Islamic principles of justice and compassion in mind.

To amplify these objectives, local imams play a pivotal role. By leveraging their moral authority and community influence, imams can integrate IDRC advocacy into their sermons and teachings. This integration allows for the reinforcement of Islamic financial ethics within a spiritual context. Imams can emphasise examples and teachings of the Prophet Muhammad (![]() ) that underscore the importance of debt repayment and financial integrity. For instance, they might quote the hadith from Sahih al-Bukhari (43:6) where the Prophet Muhammad (

) that underscore the importance of debt repayment and financial integrity. For instance, they might quote the hadith from Sahih al-Bukhari (43:6) where the Prophet Muhammad (![]() ) stated, "The best among you are those who repay debts handsomely." This teaching not only encourages prompt debt settlement but also promotes generosity and ethical conduct in financial dealings.

) stated, "The best among you are those who repay debts handsomely." This teaching not only encourages prompt debt settlement but also promotes generosity and ethical conduct in financial dealings.

By operating under this framework, the IDRC can effectively address the complex issues surrounding inheritance and debt in Muslim communities, promoting financial responsibility, ethical practices, and adherence to Islamic principles.

Framework for the Project

1. Educational Groundwork

The successful implementation of the IDRC hinges on robust community education rooted in Islamic principles. Central to this effort is the teachings of Islam about debt ethics in the masājid especially at Friday khutab, where imams can elucidate Quranic injunctions such as “If someone is in hardship, postpone repayment until ease” (Quran 2:280). Such khutab can serve as a moral compass, reinforcing the spiritual consequences of unresolved debts—such as the Prophet’s (![]() ) refusal to pray over-indebted individuals until obligations were met . By contextualizing debt resolution within Islamic teachings, imams can inspire congregants to prioritise ethical financial practices and document transactions, aligning with Quranic directives to “commit loans to writing” (Quran 2:282).

) refusal to pray over-indebted individuals until obligations were met . By contextualizing debt resolution within Islamic teachings, imams can inspire congregants to prioritise ethical financial practices and document transactions, aligning with Quranic directives to “commit loans to writing” (Quran 2:282).

Complementing this, workshops led by appropriate experts can demystify Islamic inheritance laws and debt documentation. Such community events would train participants in drafting Sharia-compliant wills and recording debts through written contracts. Practical modules might include case studies on estate management and role-playing exercises to navigate familial disputes, ensuring heirs understand their duty to settle debts from the deceased’s estate. Such initiatives address the alarming statistic that 56% of UK Muslims lack wills, mitigating risks of intestacy and unresolved liabilities.

2. Collaborative Infrastructure

A unified approach between Islamic institutions is critical. The local Council of Mosques should issue standardized guidelines for debt resolution, including templates for loan agreements and protocols for mediating disputes. By coordinating with local masājid, the Council can ensure consistency in messaging, such as distributing multilingual resources on inheritance planning and hosting quarterly seminars on financial literacy emphasising transparency and communal trust .

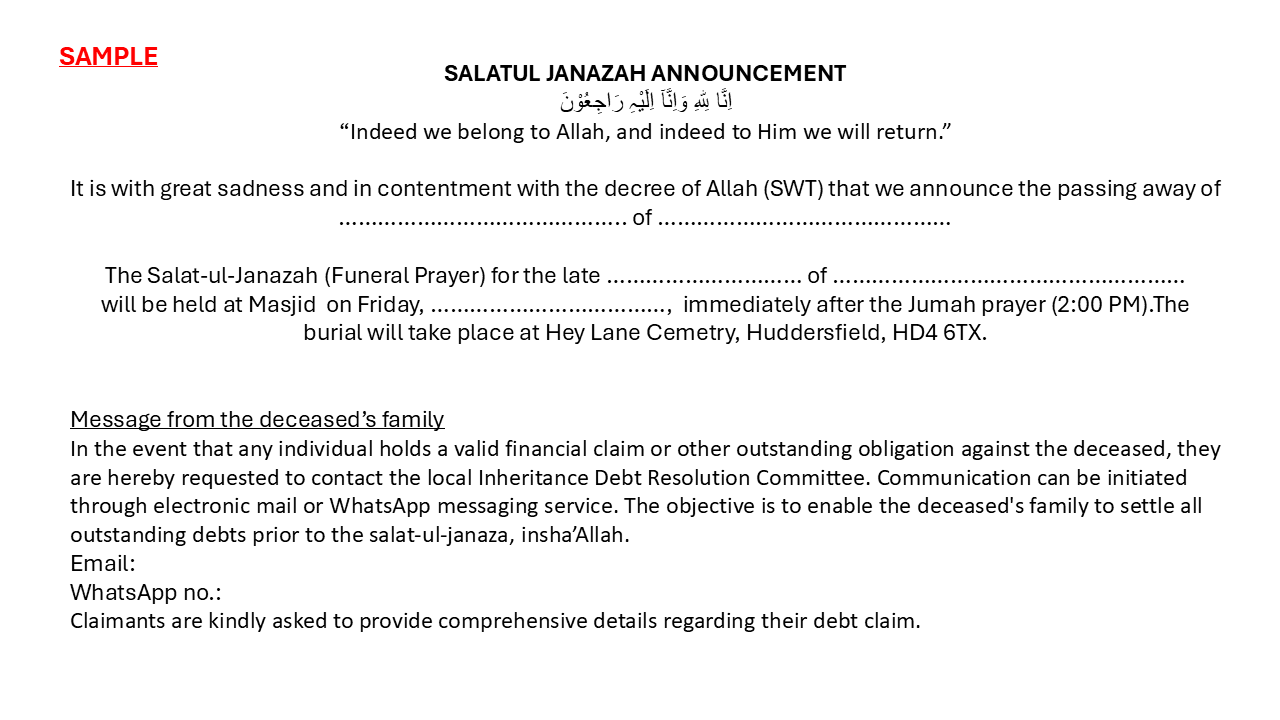

Simultaneously, the local Muslim Burial Council (local MBC) will need to integrate IDRC protocols into burial processes. Upon notification of a death, the local MBC would sensitively enquire if families wish to include a debt claim clause in the death and janaza prayer announcement, allowing creditors to come forward. Validated claims can then be prioritised ideally before burial rites, adhering to the Prophet’s (![]() ) emphasis on resolving debts promptly to free the deceased’s soul. In cases where estates are insufficient, the local IDRC could collaborate with any local or national zakat charities to explore Sharia-compliant solutions, such as voluntary repayment by heirs or creditor forgiveness .

) emphasis on resolving debts promptly to free the deceased’s soul. In cases where estates are insufficient, the local IDRC could collaborate with any local or national zakat charities to explore Sharia-compliant solutions, such as voluntary repayment by heirs or creditor forgiveness .

By intertwining education with institutional cooperation, the IDRC fosters a culture of accountability, ensuring debts are settled with dignity and aligning communal practices with Quranic justice.

Implementation of the Project

The local Muslim Burial Council (local MBC) would need to play a pivotal role in initiating the debt resolution process. Upon notification of a death, the local MBC sensitively inquires whether the family wishes to include an optional debt claim clause in public death announcements. This clause allows creditors to come forward while respecting the bereaved family’s privacy and emotional state. By framing this step as voluntary, the local MBC upholds Islamic principles of compassion and avoids adding undue stress during a period of grief.

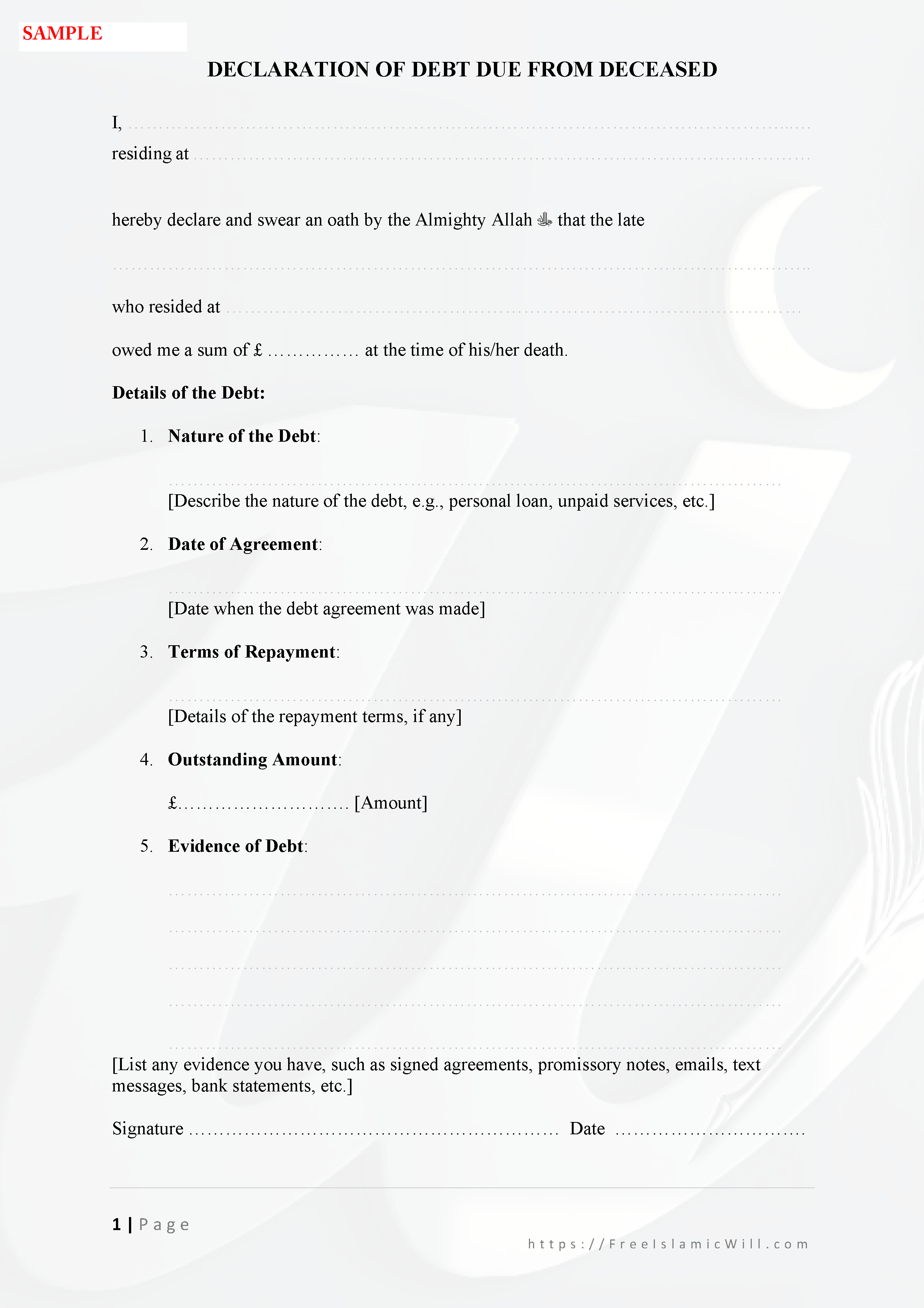

Once the announcement is disseminated, creditors are directed to submit claims through standardized IDRC forms, which require detailed evidence such as written contracts, witness statements, or transaction records. This formal process ensures accountability and reduces disputes, aligning with the Quranic mandate to “reduce debts to writing” (Quran 2:282). The IDRC reviews each claim meticulously, verifying its authenticity against submitted documentation before proceeding.

Following validation, the IDRC would notify the deceased’s family of all verified claims, providing a transparent summary of outstanding debts. This step ensures heirs are fully informed of their obligations under Islamic inheritance laws, which prioritise debt settlement before asset distribution (Quran 4:11–12). Clear communication fosters trust and encourages prompt resolution, minimising the risk of unresolved liabilities affecting the deceased’s spiritual status.

As the system evolves, the IDRC may expand its services to include mediation or arbitration, modelled on established conflict-resolution frameworks. Trained mediators would facilitate negotiations between creditors and families, aiming for equitable solutions such as extended repayment timelines or partial debt forgiveness. This phased approach not only addresses immediate concerns but also cultivates a culture of ethical financial conduct within the community, reinforcing the Prophetic teaching to “relieve the debtor with ease” (Sahih al-Bukhari 2397).

The final goal should be to establish a system within the community so that the debts of a deceased can be paid by a community fund (analogous to a bayt-ul-mal). This was the practice of the Prophet Muhammad (![]() ) when he was in a position to do so.

) when he was in a position to do so.

The Role of Zakat Funds in Settling Debts

The use of zakat to settle a deceased Muslim’s debts is governed by nuanced juristic principles, with rulings varying across Islamic schools of thought. Under Maliki and Shafi’i jurisprudence, zakat may be allocated to clear debts if the deceased was eligible for zakat during their lifetime and the debt was incurred for lawful purposes. These schools interpret Quranic injunctions broadly, emphasising communal welfare (maslaha) and the Quranic directive to aid “those in debt” (Quran 9:60). For instance, Imam al-Dardir of the Maliki school affirmed that zakat could discharge a deceased’s lawful debt if the estate is insufficient.

Conversely, the Hanafi and Hanbali schools restrict zakat disbursement to living recipients, arguing that posthumous debt relief does not directly benefit the deceased, who no longer bears worldly obligations. However, they permit voluntary repayment by heirs or third parties as an act of charity (sadaqah), reflecting the Prophetic teaching: “Whoever relieves a believer’s distress, Allāh (![]() ) will relieve theirs on the Day of Resurrection” (Sahih Muslim 2699).

) will relieve theirs on the Day of Resurrection” (Sahih Muslim 2699).

IDRC could establish a zakat subcommittee to assess eligibility. This body would verify whether the deceased met zakat criteria and mediate between creditors and heirs. Scholars like Ibn Qudamah, a prominent Hanbali jurist, endorsed such communal efforts, noting that debt relief aligns with Islam’s emphasis on collective responsibility and social harmony. By integrating these principles, the IDRC ensures adherence to Sharia while addressing the ethical imperative to safeguard the deceased’s spiritual and financial legacy.

Some FAQs related to using zakat funds to pay debts of the deceased.

Q. If Zakat requires transferring ownership to a living recipient (tamleek), how can it be used for someone who has passed away?

A. The scholars (Malaki and some Shafi’i) who consider it permissible to use zakat funds argue that paying off the debt benefits the living creditors. In essence, the zakat is not given to the deceased, but for the release of his obligations, which in turn benefits those who are alive and owed the money.

It's crucial that the deceased was eligible to receive zakat at the time of his/ her death. There are absolutely no assets in the estate to cover the debt, and the heirs are unable to pay the debt of the deceased. Some scholars further stipulate that the creditors themselves must also be eligible to receive zakat. Using zakat funds for its purpose is the last resort.

The donor of zakat funds must have the intention of relieving the hardship of the deceased and to benefit the living creditors.

Conclusion

Unresolved debts jeopardise spiritual and familial harmony, violating Islamic principles of justice. The establishment of a local IDRC offers a faith-compliant solution, uniting masājid, burial councils, and scholars to uphold Quranic mandates. By prioritising documentation, education, and mediation, the IDRC would try to ensure debts are settled with dignity.

Implementing this proposal requires sustained collaboration, but its success would affirm the Muslim community’s commitment to financial integrity and divine accountability. As the Prophet (![]() ) taught us, “Relieve the debtor, and Allāh (

) taught us, “Relieve the debtor, and Allāh (![]() ) will relieve you in this world and the next” (Sahih Muslim 2699).

) will relieve you in this world and the next” (Sahih Muslim 2699).

Dr. A. Hussain Feb. 2025

----------------------------------------------

بِسۡمِ اللهِ الرَّحۡمٰنِ الرَّحِيۡمِ

وراثتی قرضوں کے حل کے لیے مقامی کمیٹی کا قیام

یہ ایک ابتدائی تجویز ہے جو مقامی مسلم تدفین کمیٹیوں، مساجد کی کونسلوں، اور انفرادی مساجد کے لیے پیش کی جا رہی ہے کہ وہ ایک "وراثتی قرضوں کے حل کی کمیٹی" (Inheritance Debt Resolution Committee – IDRC) کے قیام پر غور کریں، تاکہ وفات پانے والے افراد کے ذمے باقی رہ جانے والے قرضوں کو فوری اور مؤثر انداز میں حل کیا جا سکے۔ یہ مجوزہ کمیٹی مسلمانوں کی کمیونٹیز میں قرضوں کی ادائیگی کے موجودہ نظام میں موجود کئی اہم مسائل کو حل کرنے کے لیے تشکیل دی جائے گی۔

براہ کرم نوٹ کریں کہ یہ ایک مسودہ تجویز ہے۔ آپ کی رائے اور تجاویز کا خیرمقدم کیا جائے گا، جنہیں ویب سائٹ یا ای میل کے ذریعے ahussain1999@doctors.org.uk پر بھیجا جا سکتا ہے۔

تعارف

اسلام میں قرض محض مالی ذمہ داری نہیں، بلکہ ایک گہری اخلاقی اور روحانی ذمہ داری ہے۔ نبی کریم ﷺ نے فرمایا:

"مؤمن کی جان اس وقت تک معلق رہتی ہے جب تک کہ اس کا قرض ادا نہ کر دیا جائے۔"

(ترمذی، کتاب 7، حدیث 49)

ایک اور حدیث میں فرمایا:

"قسم ہے اُس ذات کی جس کے ہاتھ میں محمد کی جان ہے! اگر کوئی شخص اللہ کے راستے میں شہید ہو، پھر زندہ کیا جائے، پھر شہید ہو، پھر زندہ کیا جائے، اور پھر شہید ہو، مگر اُس پر قرض باقی ہو تو جب تک وہ قرض ادا نہ کیا جائے، وہ جنت میں داخل نہیں ہوگا۔"

(احمد، مشکوٰۃ المصابیح 2929)

یہ روحانی شدت ہمیں قرض کی فوری ادائیگی کی اہمیت کا احساس دلاتی ہے، تاکہ وفات پانے والے کی آخرت کا سفر آسان ہو۔ قرآن مجید میں قرض کی تحریری دستاویز پر زور دیتے ہوئے فرمایا گیا:

"جب تم ایک مقررہ مدت تک کے لیے قرض کا معاملہ کرو تو اُسے لکھ لیا کرو۔"

(البقرہ: 282)

وراثتی قرض سے مراد وہ قرض ہے جو کسی شخص کے انتقال کے بعد اس کی جائیداد سے ادا کیا جانا ضروری ہے، قبل اس کے کہ باقی ترکہ وارثوں میں تقسیم کیا جائے۔ شریعت میں وفات پانے والے کے قرض کو ادا کرنا وراثت کی تقسیم سے بھی پہلے لازم سمجھا گیا ہے۔

ایسی صورت حال میں مقامی "وراثتی قرضوں کے حل کی کمیٹی" کا قیام اسلامی تعلیمات کے عین مطابق ہے، جو ایک منظم نظام فراہم کرے گی تاکہ باقی رہ جانے والے قرضے حل ہو سکیں۔ یہ کمیٹی دینی اداروں کی زیر نگرانی کام کرتے ہوئے، کمیونٹی کی اجتماعی ذمہ داری کو اجاگر کرے گی، خاندانی تنازعات کو کم کرے گی، اور قرآنی حکم "نیکی اور تقویٰ کے کاموں میں ایک دوسرے کا ساتھ دو" (المائدہ: 2) پر عمل پیرا ہو گی۔

مسئلے کی نوعیت اور اہمیت

برطانیہ میں 56 فیصد سے زائد افراد بغیر کسی معتبر وصیت کے وفات پاتے ہیں، جس سے وراثت کی تقسیم مزید پیچیدہ ہو جاتی ہے۔ مسلم کمیونٹی میں غیر رسمی قرضوں کا رواج اس مسئلے کو مزید گھمبیر بنا دیتا ہے، کیونکہ اکثر لین دین تحریری نہیں ہوتا، جو کہ قرآنی احکامات کے برخلاف ہے۔ ایسے معاملات میں خاندانوں کو قرض کا علم ہی نہیں ہوتا، جس سے شریعت کی وراثتی حدود (سورہ نساء: 11–12) کی خلاف ورزی کا اندیشہ ہوتا ہے۔

نتیجتاً، قرض خواہ غیر یقینی کا شکار رہتے ہیں، جبکہ وارثوں پر غیر واضح مالی ذمہ داریاں باقی رہتی ہیں۔ نبی کریم ﷺ نے اجتماعی ذمہ داری پر زور دیتے ہوئے ایسے شخص کی نماز جنازہ ادا کرنے سے انکار فرمایا جس کے ذمے قرض تھا، یہاں تک کہ کسی صحابی نے وہ قرض ادا کر دیا (مسند احمد 3/629)۔

اگر ان معاملات کو باقاعدہ نظام کے تحت حل نہ کیا جائے تو نہ صرف مرنے والے کی روح معلق رہتی ہے بلکہ خاندانوں کو بھی مالی اور ذہنی اذیت کا سامنا کرنا پڑتا ہے۔

مسئلے کے حل کے لیے تجویز

اس مسودے میں تجویز پیش کی گئی ہے کہ مقامی سطح پر "وراثتی قرضوں کے حل کی کمیٹیاں" (IDRC) قائم کی جائیں، جو مقامی مساجد کی کونسل، مسلم تدفین کمیٹی (MBC)، اور مقامی ائمہ کرام کے اشتراک سے کام کریں۔ یہ شراکت دارانہ منصوبہ مقامی مسلمانوں کے تمام قرضوں کی جلد اور منصفانہ ادائیگی کو یقینی بنائے گا، کیونکہ یہ کمیونٹی ڈھانچے اور دینی اتھارٹی سے جڑا ہو گا، جو اسے قابلِ اعتماد اور مؤثر بنائے گا۔

IDRC کے تین بنیادی مقاصد ہوں گے:

مسلمانوں کو قرض کے معاملات کو تحریری شکل دینے کی ترغیب دینا، جیسا کہ قرآن (البقرہ: 282) میں حکم دیا گیا، تاکہ شفافیت اور تنازعات سے بچاؤ ممکن ہو۔

اسلامی وراثتی قوانین اور انگلش قانون کے تحت قابلِ قبول اسلامی وصیت کی اہمیت پر آگاہی مہمات، ورکشاپس، اور سیمینارز کا انعقاد۔

ایک ثالثی کردار ادا کرنا، جہاں قرض خواہ اور لواحقین کے درمیان معاملات کو شریعت کے مطابق نرمی اور عدل سے طے کیا جائے۔

ان مقاصد کو مؤثر بنانے کے لیے مقامی ائمہ کلیدی کردار ادا کریں گے۔ اپنے خطبات اور دروس میں وہ اس مسئلے کی اہمیت کو اجاگر کر سکتے ہیں۔ مثلاً وہ صحیح بخاری (کتاب 43، حدیث 6) کی حدیث کو بیان کر سکتے ہیں:

"تم میں سب سے بہتر وہ ہے جو قرض کو خوش دلی سے ادا کرے۔"

یہ تعلیم قرض کی فوری ادائیگی اور اخلاقی مالی برتاؤ کی ترغیب دیتی ہے۔

اس نظام کے تحت IDRC نہ صرف وراثت اور قرض سے متعلق مسائل کو حل کرے گی بلکہ اسلامی اصولوں کے مطابق معاشی دیانت داری کو فروغ دے گی۔

منصوبے کا فریم ورک

1. تعلیمی بنیاد

IDRC کے کامیاب نفاذ کے لیے دینی تعلیم کا مضبوط نظام ضروری ہے۔ خاص طور پر جمعہ کے خطبات میں ائمہ کرام قرآنی آیات جیسے

"اگر قرض دار تنگ دست ہو تو اُسے مہلت دو"

(البقرہ: 280)

بیان کر کے، قرض کے اخلاقی پہلو کو اجاگر کریں۔ نبی کریم ﷺ کا قرض دار کے لیے نماز جنازہ نہ پڑھانا ایک مضبوط روحانی پیغام ہے، جو عوام کو مالی معاملات کو درست رکھنے کی ترغیب دیتا ہے۔

اس کے ساتھ، ماہرین کی زیر قیادت ورکشاپس کا انعقاد کیا جا سکتا ہے جن میں شریعت کے مطابق وصیت لکھنے، قرض کو تحریری طور پر محفوظ کرنے، اور وراثتی تنازعات سے نمٹنے کی تربیت دی جائے گی۔ عملی مشقیں، کیس اسٹڈیز، اور رول پلے سیشنز کے ذریعے افراد کو تیار کیا جائے گا کہ وہ وفات پانے والے کے قرض کو صحیح طریقے سے ادا کریں۔

2. ادارہ جاتی تعاون

مساجد کی مقامی کونسل کو چاہیے کہ قرضوں سے متعلق معیاری ہدایات، معاہدہ جات کے نمونے، اور ثالثی کے اصول جاری کرے۔ ہر مسجد میں یکساں پیغام رسانی کے لیے معلوماتی مواد تقسیم کیا جائے، اور ہر سہ ماہی میں مالی شفافیت پر سیمینارز رکھے جائیں۔

اسی طرح، مسلم تدفین کمیٹی (MBC) کو چاہیے کہ تدفین کے نظام میں IDRC کے اصولوں کو شامل کرے۔ موت کی اطلاع پر لواحقین سے نرمی سے پوچھا جائے کہ کیا وہ اعلان میں قرض کی اطلاع شامل کرنا چاہتے ہیں، تاکہ اگر کوئی قرض خواہ ہو تو وہ آگے آ سکے۔ اگر جائیداد ناکافی ہو تو IDRC مقامی یا قومی زکوٰۃ اداروں سے مدد لے سکتی ہے تاکہ قرض کی ادائیگی کسی شرعی طریقے سے ممکن ہو جائے۔

تعلیم اور ادارہ جاتی ہم آہنگی کے ذریعے IDRC کمیونٹی میں احتساب، شرافت اور دینی شعور پیدا کرے گی۔

منصوبے کا نفاذ

مقامی مسلم تدفین کمیٹی (MBC) اس منصوبے کو عملی طور پر شروع کرنے میں اہم کردار ادا کرے گی۔ جب کسی مسلمان کے انتقال کی اطلاع ملے، تو MBC نرمی سے پوچھے کہ کیا خاندان موت کے اعلان میں قرض سے متعلق ایک اختیاری شق شامل کرنا چاہتا ہے۔ اس شق کے ذریعے قرض خواہوں کو موقع دیا جائے گا کہ وہ اپنے مطالبات پیش کر سکیں، جبکہ مرحوم کے اہلِ خانہ کے غم و جذبات کا بھی لحاظ رکھا جائے گا۔

اس عمل کو اختیاری رکھ کر MBC اسلامی شفقت کے اصولوں پر کاربند رہے گی اور غم کی حالت میں خاندان پر اضافی دباؤ ڈالنے سے گریز کرے گی۔

اعلان کے بعد اقدامات

جب قرض کی اطلاع کے لیے اعلان جاری کر دیا جاتا ہے، تو قرض خواہوں کو ہدایت دی جاتی ہے کہ وہ مخصوص IDRC (وراثتی قرض حل کمیٹی) کے فارم کے ذریعے اپنے دعوے جمع کروائیں۔ ان فارمز میں تفصیلی شواہد جیسے تحریری معاہدے، گواہوں کے بیانات، یا مالی لین دین کے ریکارڈ شامل کرنا لازمی ہوتا ہے۔ یہ باضابطہ طریقہ کار جواب دہی کو یقینی بناتا ہے اور تنازعات کو کم کرتا ہے، جیسا کہ قرآن مجید میں فرمایا گیا: "قرض کو لکھ لیا کرو" (البقرہ 2:282)۔

IDRC ہر دعوے کا باریک بینی سے جائزہ لیتی ہے اور جمع شدہ دستاویزات کی بنیاد پر اس کی تصدیق کرتی ہے۔ تصدیق کے بعد، کمیٹی مرحوم کے اہل خانہ کو تمام منظور شدہ دعووں سے آگاہ کرتی ہے اور واجب الادا قرضوں کی شفاف فہرست فراہم کرتی ہے۔ یہ اقدام ورثاء کو ان کی شرعی ذمہ داریوں سے مکمل طور پر باخبر کرتا ہے، کیونکہ شریعت کے مطابق ترکے کی تقسیم سے قبل قرضوں کی ادائیگی لازم ہے (النساء 4:11–12)۔

واضح رابطے اعتماد کو فروغ دیتے ہیں اور قرضوں کے جلد حل کی ترغیب دیتے ہیں، تاکہ مرحوم کی روح پر کوئی بوجھ باقی نہ رہے۔

ثالثی اور بقایا جات کا حل

وقت کے ساتھ، IDRC اپنی خدمات کو ثالثی اور مصالحت تک وسعت دے سکتی ہے، جیسا کہ دیگر تنازع حل کرنے والے اداروں میں ہوتا ہے۔ تربیت یافتہ ثالثین قرض دہندگان اور لواحقین کے درمیان مذاکرات میں سہولت فراہم کریں گے، تاکہ واجب الادا قرضوں کے لیے مناسب اقساط یا جزوی معافی جیسے متوازن حل ممکن ہو سکیں۔

یہ تدریجی طریقہ صرف فوری مسائل کو حل نہیں کرتا بلکہ کمیونٹی میں مالیاتی اخلاقیات کا ایک مثبت ماحول بھی تشکیل دیتا ہے، جیسا کہ رسول اللہ ﷺ نے فرمایا: "قرض دار کو آسانی فراہم کرو" (صحیح بخاری 2397)۔

کمیونٹی فنڈ اور بیت المال کی طرز پر نظام

آخری ہدف یہ ہونا چاہیے کہ کمیونٹی میں ایسا نظام قائم ہو جائے جس کے ذریعے کسی مرحوم کا قرض بیت المال جیسے فنڈ سے ادا کیا جا سکے۔ جب رسول اللہ ﷺ کو موقع میسر آیا تو آپ ﷺ نے یہی عمل فرمایا۔

زکوٰۃ فنڈ کے ذریعے قرض کی ادائیگی

زکوٰۃ کے ذریعے مرحوم کے قرض کی ادائیگی ایک فقہی مسئلہ ہے، جس میں مختلف مکاتبِ فکر کی آراء پائی جاتی ہیں۔

مالکی اور شافعی فقہ کے مطابق، اگر مرحوم اپنی زندگی میں زکوٰۃ کا مستحق تھا اور قرض جائز مقصد کے لیے لیا گیا تھا تو اس کی ادائیگی زکوٰۃ سے کی جا سکتی ہے۔ یہ مکاتب قرآن مجید کی ہدایت "اور قرض داروں کو دو" (التوبہ 9:60) کو وسیع معنوں میں لیتے ہیں۔

مثال کے طور پر، امام دردیر (مالکی فقہ) فرماتے ہیں کہ اگر مرحوم کی جائیداد ناکافی ہو تو زکوٰۃ سے جائز قرض ادا کیا جا سکتا ہے۔

حنفی اور حنبلی فقہ زکوٰۃ کو صرف زندہ مستحقین کے لیے مخصوص سمجھتے ہیں۔ ان کے نزدیک، فوت شدہ شخص کے لیے زکوٰۃ سے براہِ راست فائدہ ممکن نہیں کیونکہ وہ دنیاوی مکلف نہیں رہا۔ البتہ، وہ ورثاء یا تیسرے افراد کی طرف سے بطور صدقہ قرض ادا کرنے کو جائز سمجھتے ہیں، جیسا کہ نبی کریم ﷺ نے فرمایا: "جو کسی مومن کی تنگی دور کرے، اللہ اس کی قیامت کے دن تنگی دور فرمائے گا" (صحیح مسلم 2699)۔

IDRC ایک زکوٰۃ ذیلی کمیٹی قائم کر سکتی ہے جو مرحوم کی اہلیت کا جائزہ لے اور قرض خواہوں اور ورثاء کے درمیان ثالثی کرے۔ علامہ ابن قدامہ جیسے جلیل القدر حنبلی علماء اس طرح کی اجتماعی کوششوں کی تائید کرتے ہیں کیونکہ یہ دین کی اجتماعی فلاح اور اخوت کی تعلیمات سے ہم آہنگ ہیں۔

زکوٰۃ سے قرض کی ادائیگی کے متعلق عام سوالات

سوال: اگر زکوٰۃ کی ادائیگی زندہ فرد کی ملکیت میں منتقل (تملیک) کیے بغیر درست نہیں، تو اسے مرحوم کے لیے کیسے استعمال کیا جا سکتا ہے؟

جواب: جن فقہاء (مالکی اور بعض شافعی) کے نزدیک یہ جائز ہے، ان کے مطابق قرض کی ادائیگی زندہ قرض خواہوں کے فائدے کے لیے کی جاتی ہے۔ دراصل زکوٰۃ مرحوم کو نہیں دی جاتی بلکہ اس کے ذمہ کے خاتمے کے لیے دی جاتی ہے، جس کا فائدہ زندہ افراد کو ہوتا ہے۔

شرط یہ ہے کہ مرحوم اپنی وفات کے وقت زکوٰۃ کا مستحق ہو، اس کی جائیداد قرض چکانے کے لیے ناکافی ہو، اور ورثاء ادائیگی کے قابل نہ ہوں۔ بعض علماء مزید یہ شرط رکھتے ہیں کہ قرض خواہ بھی زکوٰۃ کے مستحق ہوں۔ زکوٰۃ کو اس مقصد کے لیے استعمال کرنا آخری حل ہونا چاہیے۔

زکوٰۃ دینے والے کو نیت یہ رکھنی چاہیے کہ وہ مرحوم کی مشکلات کو آسانی میں بدلنے اور زندہ قرض خواہوں کو فائدہ پہنچانے کے لیے زکوٰۃ دے رہا ہے۔

اختتامیہ

غیر ادا شدہ قرض روحانی اور خاندانی توازن کو خطرے میں ڈالتا ہے، اور اسلامی عدل کے اصولوں کی خلاف ورزی ہے۔ مقامی وراثتی قرض حل کمیٹی (IDRC) کا قیام ایک شرعی اور عملی حل پیش کرتا ہے جو مساجد، تدفین کونسلوں اور علماء کو متحد کرتا ہے تاکہ قرآنی احکامات پر عمل ہو سکے۔

دستاویزی عمل، تعلیم اور ثالثی کو بنیاد بنا کر یہ کمیٹی یقینی بنائے گی کہ قرض باعزت طریقے سے ادا ہو جائے۔

اس منصوبے کی کامیابی طویل المدتی تعاون پر منحصر ہے، لیکن اس کا قیام مسلم کمیونٹی کی مالی دیانت اور دینی جواب دہی سے وابستگی کو ظاہر کرے گا۔ جیسا کہ نبی کریم ﷺ نے فرمایا:

"جو کسی مقروض کو راحت دے، اللہ اسے دنیا و آخرت میں راحت عطا کرے گا" (صحیح مسلم 2699)۔